Understanding the Debt Trap

Introduction

The term “debt trap” describes a situation where the money you owe keeps growing instead of shrinking, even though you are making payments. For many people, especially credit card users, this can feel confusing. “How can I be paying every month but still owe more?” The answer lies in how interest works.

This article explains the concept of a debt trap in India in simple words. We’ll look at why paying only the minimum amount due is dangerous, how interest compounds, and what steps can help you escape. At the end, you can also try our Debt Trap Quiz to see this concept in action.

What Is a Debt Trap?

A debt trap occurs when:

- You borrow money (for example, through a credit card).

- You don’t repay the full amount.

- The unpaid part is charged high interest every month.

- As a result, your balance grows instead of reducing.

The key idea is this: when interest charges are bigger than the payments you make, your debt increases over time.

This is why many households find themselves stuck in what is called a debt trap in India.

The Role of Minimum Payment

Credit card statements show a “minimum amount due,” usually 5% of the total bill. Many people believe paying this is enough. In reality, this is the trap.

Example:

- Your spending = ₹10,000

- Minimum due (5%) = ₹500

- Unpaid amount = ₹9,500

- Interest charged = 3% per month (~36% annually)

- Next month balance = ₹9,785

Even after paying, your balance has only reduced slightly. If you repeat this every month, the debt hardly reduces and the interest keeps piling up.

This is the mathematics of the debt trap.

How Interest Compounds

The reason debt grows fast is because of compound interest. This means:

- Month 1: You are charged interest on the unpaid balance.

- Month 2: Interest is charged not just on the original debt, but also on the previous interest.

So, your debt keeps “compounding” or multiplying.

For example, if you owe ₹20,000 and don’t pay in full:

- At 3% monthly interest, that’s ₹600 in interest every month.

- If you only pay ₹1,000, the remaining balance is still high.

- By the end of 12 months, you could owe much more than what you started with.

This is how people unknowingly fall into a debt trap in India.

Example Simulation

Let’s use a simple case:

- Starting debt: ₹10,000

- Interest rate: 3% per month

- Payment each month: ₹500 (minimum due)

| Month | Opening Balance | Payment | Interest (3%) | Closing Balance |

|---|---|---|---|---|

| 1 | ₹10,000 | ₹500 | ₹285 | ₹9,785 |

| 2 | ₹9,785 | ₹500 | ₹278 | ₹9,563 |

| 3 | ₹9,563 | ₹500 | ₹269 | ₹9,332 |

Notice: After paying ₹1,500 across 3 months, your balance has reduced by only ₹668. Most of your payment went into covering interest.

This is the essence of the debt trap — you pay, but progress is slow because interest eats up most of your money.

Why the Debt Trap Feels Invisible

Many people don’t realize they are in a trap because:

- The minimum due looks affordable.

- The balance reduces very slowly, so it feels like you are paying.

- Interest charges are added silently every month.

But behind the scenes, the unpaid portion keeps growing due to compounding.

This is why understanding the concept of debt trap in India is important for financial literacy.

Breaking the Cycle

The only way to escape a debt trap is to break the cycle of compounding interest. This means:

- Pay more than the minimum – Try to pay at least 50% of your balance.

- Clear the full amount if possible – This stops interest immediately.

- Avoid new borrowing until old debt is cleared.

Remember: every extra rupee you pay above the minimum goes directly toward reducing the principal balance, which lowers future interest.

Educational Analogy

Think of debt like a bucket with a hole.

- The money you pay is water poured into the bucket.

- The hole is the interest rate.

- If you pour in very little water (minimum due), most leaks out through the hole, and the bucket never fills.

- If you pour in enough water (full payment), you block the hole, and the bucket fills up.

This simple analogy explains why only paying the minimum keeps you stuck in a debt trap.

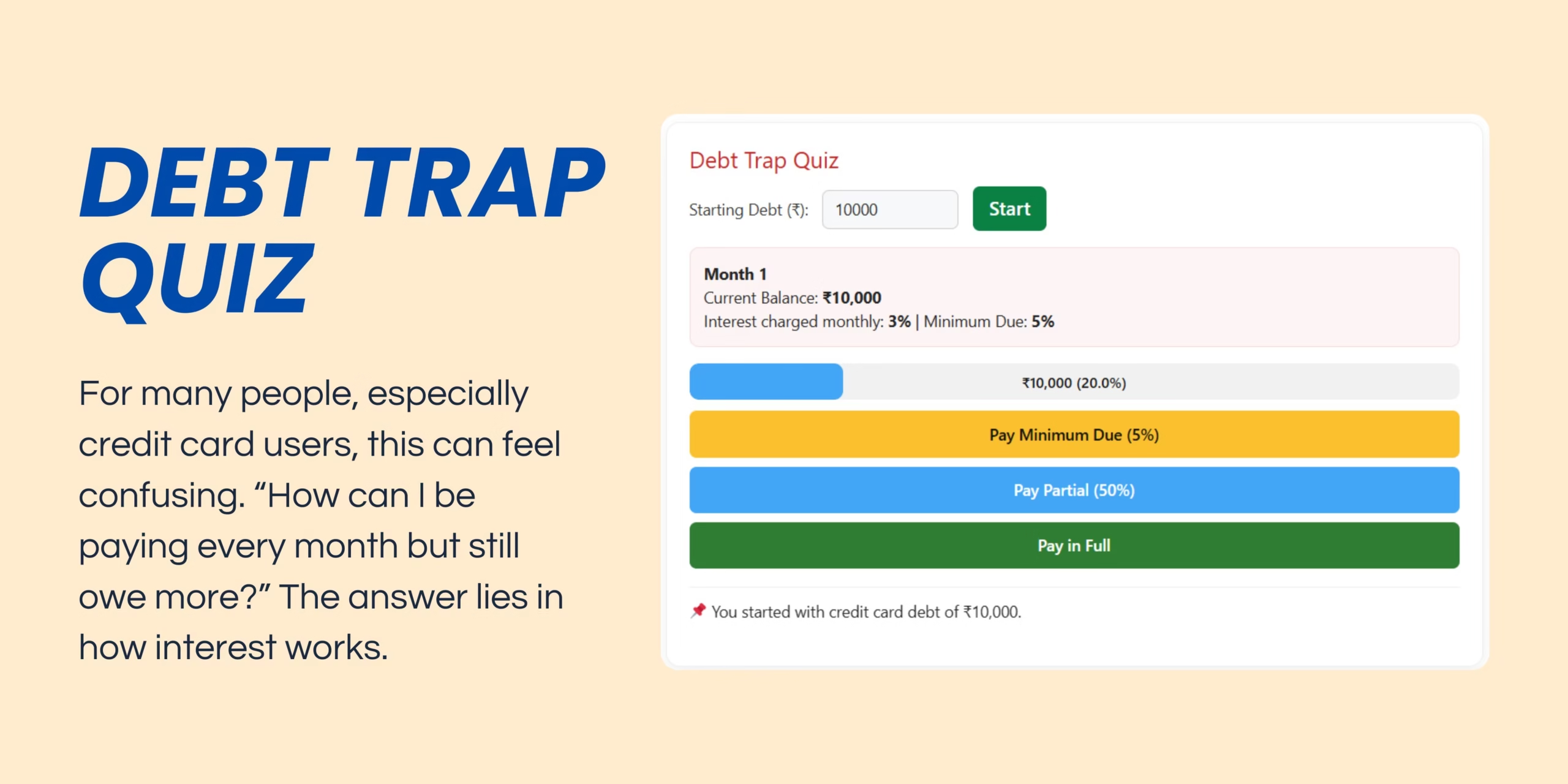

Play the Debt Trap Quiz

Theory is easier to understand with practice. Our Debt Trap Quiz lets you:

- Enter your own debt amount (e.g., ₹10,000).

- Choose whether to pay the minimum, half, or full balance.

- Watch an animated bar showing how the debt grows or reduces each month.

This interactive tool helps you see the concept of the debt trap in India in action.

Disclaimer

This quiz assumes:

- 3% monthly interest (~36% annually)

- 5% minimum due

- ₹50,000 danger threshold

These are based on typical credit card terms in India. Actual charges may differ. The example is for educational purposes only and not financial advice.

Conclusion

A debt trap is not about bad luck — it is about how interest and minimum payments interact. The trap is simple: if you only pay a little, interest keeps growing and cancels out your efforts.

The concept is easy to understand with numbers: ₹10,000 borrowed at 3% monthly interest can take years to clear if you pay only the minimum. But if you pay in full, you avoid interest altogether.

Use the Debt Trap Quiz to experience this concept visually. Once you see how quickly debt grows with minimum payments, you’ll understand why clearing balances fully is the smartest choice.