The truth is, with mindful budgeting and a few lifestyle adjustments, it is possible to save at least ₹3,000–₹6,000 each month from a ₹30000 salary without making life feel restrictive.

Many people wonder how to save money with 30000 salary, especially when expenses seem to rise as quickly as income.

At first glance, saving on 30000 salary may feel easier than on 20000, but often that’s not the case. The moment income increases, expenses also rise, to better restaurants, new gadgets, and higher rent.

It’s called lifestyle inflation, and it can swallow up your salary before you realize it.

I once knew a colleague in Pune who earned 30000 salary and still managed to save enough for an international trip within two years.

His trick wasn’t earning extra, it was learning to plan and automate his savings. That’s the kind of discipline that makes the difference.

So, let’s break down practical and human ways to save money with 30000 salary in India.

Table of Contents

Why Saving Feels Challenging on 30000 Salary

When you earn 30000, every rupee already feels allocated, rent, groceries, transport, family support, and a little for leisure.

By the time you reach the end of the month, it feels like nothing is left.

It’s like trying to fill a pot with water while tiny holes at the bottom keep draining it. The leaks are hidden, small impulse buys, subscriptions, takeouts, but over time, they add up.

Once you spot them, saving becomes easier.

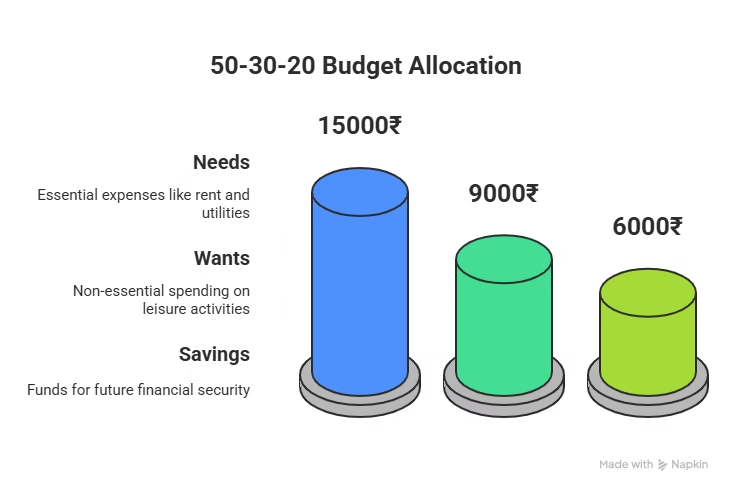

Budgeting with 30000 Salary: A Simple Framework

One practical way to handle your income is through the 50-30-20 budgeting rule. Here’s how it looks for 30000 salary:

- 50% Needs (₹15,000): Rent, groceries, utilities, transport.

- 30% Wants (₹9,000): Eating out, shopping, movies.

- 20% Savings (₹6,000): Emergency fund, RDs, SIPs.

Table 1: Example Budget for 30000 Salary

| Category | Percentage | Amount (₹) |

|---|---|---|

| Needs | 50% | 15,000 |

| Wants | 30% | 9,000 |

| Savings | 20% | 6,000 |

Even if you can’t hit 20%, starting with 10% (₹3,000) still builds momentum.

Automate and Simplify Your Savings

The best way to save money with 30000 salary is to make saving invisible. Set up an auto-transfer to a savings account or SIP on the day your salary arrives.

This way, saving becomes a habit, not a decision you negotiate every month.

Think of it as paying your future self first. Even ₹3,000 a month adds up to ₹36,000 a year, and that’s before considering interest or investment returns.

Small Lifestyle Shifts That Add Up

Saving doesn’t mean punishing yourself. It means adjusting small habits:

- Cooking at home twice a week instead of ordering food can save ₹2,000 monthly.

- Choosing buses or metros over cabs can cut commuting costs by half.

- Dropping unused subscriptions like OTT apps or gyms you rarely visit frees ₹500–₹1,000 easily.

Over time, these small changes create space for consistent savings.

Avoiding Debt Traps on 30000 Salary

Credit cards and EMIs are tempting when income rises. But debt is a silent drain. If you do use credit cards, pay the full bill on time.

If you buy something on EMI, check whether it genuinely fits your budget. Living within your means is the surest way to avoid financial stress.

Emergency Fund: The Cushion You Need

An emergency fund is your financial safety net. Even ₹1,500-₹2,000 saved monthly builds ₹18,000-₹24,000 in a year. Over time, it grows into a 3-6 month buffer that protects you from borrowing in tough times.

Thinking Beyond 30000: Side Hustles

There’s only so much you can cut. To increase savings faster, consider earning more. Freelancing, tutoring, delivery gigs, or selling skills online can bring in an extra ₹3,000-₹5,000. Combined with your salary, this boosts your saving power without cutting joys.

If you want to know more on How to Create Passive Income in India: Complete Guide for 2025

Comparison: 20000 vs 30000 Salary Savings

To connect this with the earlier salary story, here’s how savings potential compares:

Table 2: Savings Potential – 20000 vs 30000 Salary

| Salary (₹) | Suggested Savings % | Possible Monthly Savings (₹) | Annual Savings (₹) |

|---|---|---|---|

| 20000 | 10-20% | 2,000 – 4,000 | 24,000 – 48,000 |

| 30000 | 10-20% | 3,000 – 6,000 | 36,000 – 72,000 |

This shows clearly that the habit of saving matters more than the salary figure. If you couldn’t save at 20000, chances are you won’t save at 30000 unless you change your approach.

Read this if you want to know How to Save Money with 20000 Salary: Proven & Simple Ways for Smart Living

So, how to save money with 30000 salary in India? The realistic answer is by consciously setting aside ₹3,000–₹6,000 every month through smart budgeting, reducing money leaks, and building habits that support long-term financial health.

But more than numbers, it’s about mindset. The ₹30000 salary itself won’t secure your future, but the way you use it can.

Building discipline today ensures you’ll save even more when you earn ₹50,000 or ₹1,00,000.

Think of saving not as a burden, but as freedom. Every rupee saved is a step toward choices — whether that’s travel, buying a home, or simply living without financial stress.

Many people earning the same as you seem relaxed while others struggle.

Often, the difference isn’t income; it’s discipline. And that discipline is something you can start building today.

FAQs on How to Save Money with 30000 Salary

Q1. Can I save money with 30000 salary in India?

Yes. With mindful budgeting and expense control, you can save between ₹3,000 and ₹6,000 every month.

Q2. How much should I ideally save from 30000 salary?

Aim for 20% (₹6,000). But even 10% (₹3,000) is a solid start if your expenses are high.

Q3. Should I save or invest with 30000 salary?

Start with an emergency fund. Once that’s secure, invest in safe options like RDs or mutual funds.

Q4. What is the difference in savings between 20000 and 30000 salary?

At 20000, savings are about ₹2,000–₹4,000 monthly. At 30000, potential rises to ₹3,000–₹6,000 monthly — showing how habits, not just income, matter.

Disclaimer: This article is for informational purposes only. It is not financial advice. Please consult a qualified financial advisor before making money-related decisions.