Simple EMI Calculator

I remember the first time I took a loan, I focused only on the monthly EMI and didn’t pay much attention to how much of that EMI was interest. A year later I realised a large chunk of my payments was interest and that I could have saved a lot by changing the tenure.

If that sounds familiar, an EMI calculator is the small tool that would have saved me confusion (and some worry).

An EMI (Equated Monthly Instalment) calculator is simply a quick way to answer three basic questions: how much will I pay every month, how much interest will I pay in total, and what will the total outflow be over the loan’s life.

It’s a little gadget; plug in loan amount, interest rate and tenure, and you get clear numbers. No spreadsheets, no guesswork.

Table of Contents

Why an EMI calculator matters

Lots of people pick a loan by looking at the lowest rate, or the EMI amount that “fits the budget,” but not both together. An EMI calculator helps you balance the two. It lets you:

- Check affordability (can I pay this EMI every month?).

- Compare tenures (shorter tenure – higher EMI but less interest overall).

- Compare loan offers (different banks, different interest rates).

- Plan cash flow – know in advance how a new loan will affect your monthly budget.

How to use it (three simple steps)

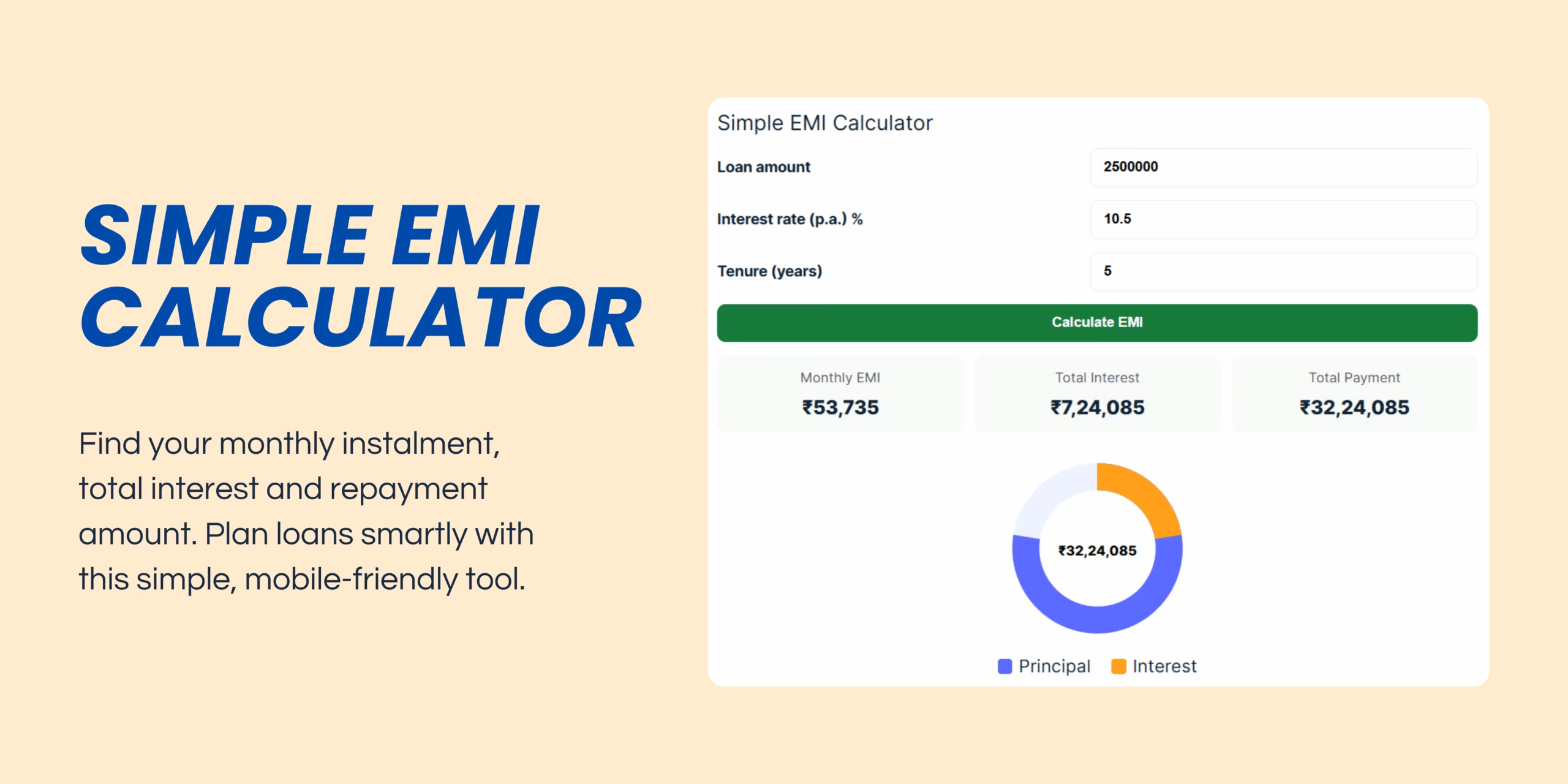

- Loan amount: the principal you want to borrow (e.g., ₹25,00,000).

- Interest rate (p.a.): the annual rate the bank charges, enter it as a percent (e.g., 10.5).

- Tenure: loan duration in years (or months if your calculator supports that).

Hit Calculate and you’ll get EMI, total interest payable and total payment.

A quick example (real numbers)

Say you borrow ₹25,00,000 at 10.5% p.a. for 5 years. When you plug these into the EMI formula, the EMI comes to about ₹53,735 per month. Over 60 months (5 years) you’ll pay roughly ₹32,24,085, which means total interest ≈ ₹7,24,085.

That example shows something important: even a seemingly small interest percent accumulates over years. If you reduce the tenure, EMI goes up but total interest falls. If you increase tenure, EMI becomes smaller but you pay more interest long-term.

Note: the calculator uses standard EMI math (monthly compounding) and gives a close estimate. Actual bank statements may differ slightly due to rounding or processing days.

Practical tips when using the EMI calculator

- Try different tenures: sometimes paying a slightly higher EMI (by choosing a shorter tenure) saves more interest than investing the same extra money elsewhere.

- Check effective rate: ask lenders about processing fees, prepayment penalties, and whether the rate is fixed or floating. Those affect final cost.

- Use it before you sign: run scenarios: best-case (lower rate), worst-case (rate hike), and realistic-case. This prepares you for surprises.

- Link to goals: if buying a house, think about how EMI fits into your long-term budget (kids’ education, emergency fund, retirement saving).

Limitations to remember

- EMI calculators assume the interest rate you enter remains constant. If you have a floating rate loan, your EMI or interest composition will change over time.

- They do not include extra charges like processing fees, insurance, or prepayment penalties unless you manually factor them in.

- EMI calculators are not financial advice: they are planning tools. Use them to inform decisions, not to replace a discussion with your bank or financial advisor where necessary.

Small but powerful

An EMI calculator doesn’t make decisions for you, but it does remove the fog. It turns complex math into clear numbers so you can ask better questions (Can I reduce tenure? Should I prepay? Which bank gives the lower overall cost?). Use it early before you sign the loan, and you’ll be in a far stronger position.

If you like, I can add a short section to this post showing an EMI vs tenure mini-table or an amortisation snippet so readers can see how the principal vs interest split changes year by year. Which would you prefer?

Check out our SIP Calculator.

2 thoughts on “EMI Calculator: How to Understand Your Loan Payments (in plain language)”