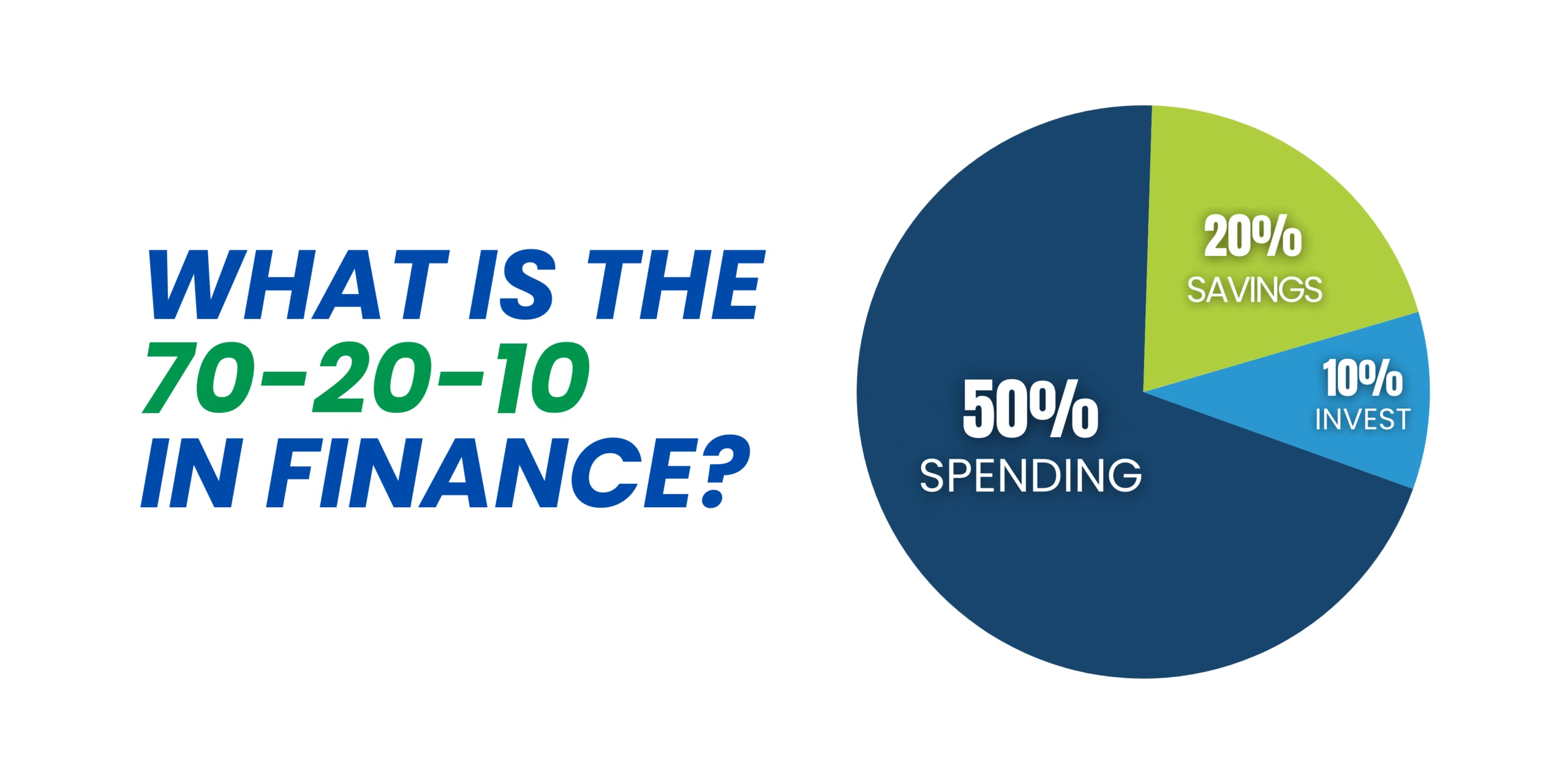

Managing money can feel overwhelming when one income must stretch across living costs, savings, and debt. Over time, experts have developed simple frameworks to help. One of the most popular is the 70 20 10 rule in finance, also called the 70 20 10 budget rule or 70 20 10 savings rule.

In simple terms, the rule suggests dividing income into:

- 70% for expenses (housing, groceries, transport, bills, insurance)

- 20% for savings and investments (mutual funds, retirement, emergency funds)

- 10% for debt repayment or charitable giving

Its appeal lies in simplicity. Unlike complex tracking apps, the 70 20 10 rule offers a quick structure that builds discipline while leaving room for flexibility.

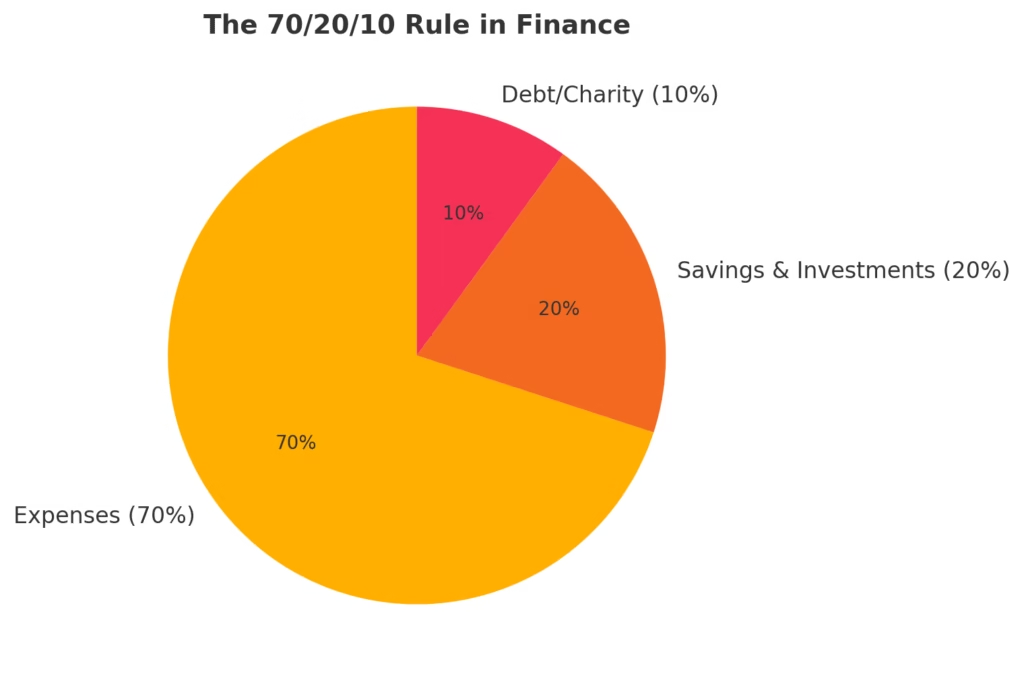

What is the 70 20 10 Rule in Finance?

The 70 20 10 rule in personal finance is a budgeting formula that divides earnings into three simple categories.

- 70% covers all living expenses: rent/mortgage, food, utilities, commuting, and other daily costs.

- 20% goes to savings or investments, such as SIPs, fixed deposits, or retirement contributions.

- 10% is reserved for repaying debt (like credit cards, personal loans) or, if debt-free, for charity or personal growth.

Compared with the 50 30 20 rule, which separates needs, wants, and savings, the 70 20 10 budgeting rule emphasizes essentials and debt responsibility over discretionary spending.

Read more to know How to Save Money with 20000 Salary

Breaking Down the Rule in Detail

- 70%: Living Expenses

Ensures lifestyle costs are capped. Includes housing, bills, groceries, insurance, and transport. - 20%: Savings & Investments

Builds wealth over time. Could include emergency funds, mutual funds, or retirement planning. - 10%: Debt Repayment / Charity

Helps manage loans while encouraging generosity or personal development.

Example for ₹50,000 monthly income:

| Category | % | Amount (₹) |

|---|---|---|

| Living Expenses | 70% | 35,000 |

| Savings & Investments | 20% | 10,000 |

| Debt / Charity | 10% | 5,000 |

Why the 70 20 10 Budget Rule Works

- Encourages balance: covers needs, builds savings, and reduces debt.

- Reduces stress: fewer categories than detailed budgets.

- Builds habits: consistency matters more than perfection.

For beginners, it’s one of the easiest financial planning strategies to follow.

Practical Example (Indian Context)

Someone earning ₹30,000 monthly can apply the 70 20 10 rule like this:

- ₹21,000 → Rent, groceries, transport

- ₹6,000 → Investments or emergency fund

- ₹3,000 → Loan EMI or donations

This shows that even at modest income levels, the framework creates savings discipline.

Comparison With Other Budgeting Rules

- 50/30/20 Rule (Thumb Rule of Personal Finance): 50% needs, 30% wants, 20% savings. More lifestyle-focused.

- 75/15/10 Plan: Used by some high-income earners — 75% spend, 15% save, 10% invest/give.

- 80/10/10 Budget: Simple version where 80% is for spending, 10% saving, 10% giving.

- Other Variants: 40/30/20/10, 60/20/20, 33/33/33 rule, etc.

The 70 20 10 rule in finance stands out because it explicitly prioritizes debt repayment/charity, which most other rules ignore.

Benefits and Limitations

Benefits

- Simple & easy to remember

- Ensures savings + debt are never ignored

- Flexible enough for any income level

Limitations

- High-cost cities may make 70% insufficient for expenses

- Heavy debt may require >10% repayment

- Doesn’t separate needs vs. wants like the 50/30/20 rule

Best viewed as a starting point, not a rigid formula. Adjust as needed.

Read this also Budgeting in India: Smart Ways to Manage Money

Free 70 20 10 Budget Template & Calculator

To make this rule practical, many people use budget calculators or Excel/Google Sheets templates.

- You can set up a simple sheet with auto-percentage formulas.

- Apps like Mint, YNAB, or Excel trackers already include versions of the 70/20/10 framework.

- For beginners, a free 70 20 10 budget template is the fastest way to test it out.

FAQs on the 70 20 10 Rule in Finance

Q1: What is the 70 20 10 rule in finance?

It’s a budgeting formula that allocates 70% to expenses, 20% to savings, and 10% to debt or giving.

Q2: Is the 70 20 10 rule better than the 50 30 20 rule?

The 70 20 10 budgeting rule is stricter on debt and savings, while 50 30 20 gives more room for lifestyle spending.

Q3: Can the 70 20 10 rule work in India?

Yes, but adjustments may be needed in metros with higher rent.

Q4: What is the difference between the 70 20 10 rule and the 80 10 10 budget?

The 70 20 10 rule prioritizes debt repayment and savings, while the 80 10 10 budget simplifies everything into spending, saving, and giving.

Q5: Is there a 70 20 10 budget calculator or template?

Yes, many free online templates and calculators help apply the rule automatically.

Q6: Who should use the 70 20 10 rule in finance?

It’s most effective for beginners or anyone seeking a simple money management formula.

The 70 20 10 rule in finance offers a simple but powerful framework to balance today’s needs with tomorrow’s security. By allocating income into expenses, savings, and debt/giving, it creates order without over-complication.

While not perfect, and often compared with the 50/30/20 rule or the 80/10/10 budget, its true value lies in adaptability. Treat it as a flexible guide to develop financial discipline, rather than a strict formula.

In a world full of uncertainty, simple strategies like the 70 20 10 savings rule can help anyone take confident steps toward stability and independence.

Disclaimer: This article is for educational purposes only. It does not provide financial advice. Readers should evaluate their own circumstances and consult certified financial planners or official resources before making financial decisions.