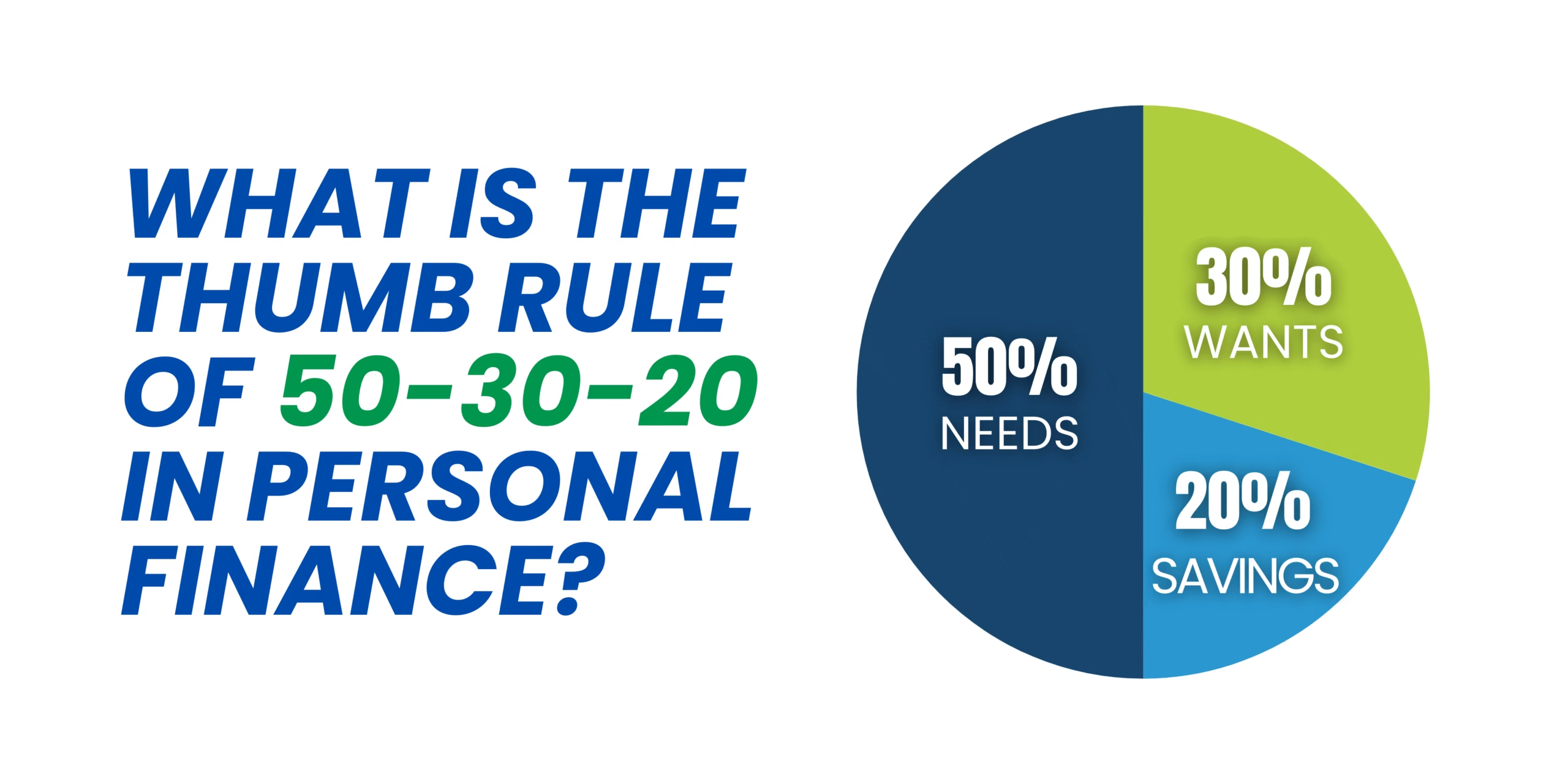

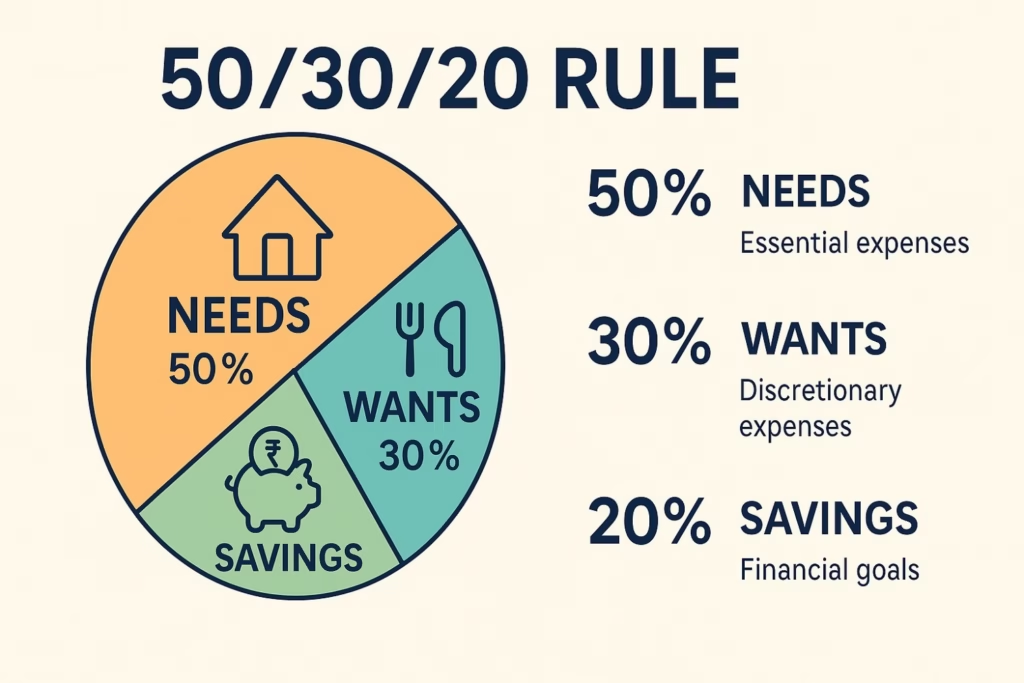

What is the thumb rule of 50 30 20 in personal finance? It is a simple budgeting guideline that suggests dividing your income into three parts: 50% for needs, 30% for wants, and 20% for savings and investments.

This thumb rule helps individuals manage money better by balancing essential expenses, lifestyle choices, and long-term financial security.

Have you ever felt that your salary disappears too quickly, leaving little to save? The 50-30-20 approach gives you a structured way to handle money without complicated spreadsheets. Think of it as slicing your income like a pizza, ensuring every piece goes to the right place.

What is the Thumb Rule of 50-30-20 in Personal Finance?

In personal finance, the 50-30-20 thumb rule is a budgeting method that divides your income into three categories:

- 50% for Needs: Basic expenses like rent, groceries, utility bills, transport, and insurance.

- 30% for Wants: Lifestyle choices like eating out, Netflix, shopping, or vacations.

- 20% for Savings & Investments: Emergency funds, retirement accounts, or mutual funds.

This rule was popularized by U.S. Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan.” Over time, it became a global reference point for beginners in personal finance.

Why Does the 50-30-20 Rule Matter?

- Simplicity: No complex spreadsheets needed. Just three broad categories.

- Balance: It ensures you enjoy life (30%) while securing your future (20%).

- Awareness: Forces you to reflect on where your money actually goes.

Think of it as traffic lights for your salary – green for savings, yellow for wants, red for needs.

Practical Example of the 50-30-20 Rule

Let’s say your monthly income is ₹40,000. Here’s how the thumb rule applies:

| Category | Percentage | Amount (₹) | Examples |

|---|---|---|---|

| Needs | 50% | 20,000 | Rent, food, transport, utilities |

| Wants | 30% | 12,000 | Eating out, movies, shopping |

| Savings | 20% | 8,000 | SIPs, RDs, emergency fund |

By following this, you’re not just surviving month-to-month, you’re actively building financial security.

Benefits of Following the 50-30-20 Thumb Rule

- Reduces Stress – Knowing exactly how much goes where keeps you in control.

- Promotes Saving Habit – Even if small, that 20% adds up over time.

- Balances Life – You can spend guilt-free on wants, knowing savings are secured.

- Adaptable – Works for salaries, business income, or even pocket money for students.

Read RBI's Financial Literacy Guide here.

Challenges & Adjustments

Of course, not everyone can strictly follow this thumb rule in personal finance. For example:

- In metro cities, needs (rent, transport) may exceed 50%.

- Students or freshers may struggle to allocate 20% to savings.

- Families with children may find their “wants” shrinking naturally.

In such cases, the percentages can be adjusted—for instance, 60-20-20 (more for needs), or 50-20-30 (higher savings goal). The thumb rule is a guide, not a law.

How to Start Using the 50-30-20 Rule Today

- Calculate your monthly take-home income.

- List out your current expenses.

- Categorize them into needs, wants, and savings.

- Adjust gradually instead of overnight cuts.

- Automate savings so that the 20% is secured before spending begins.

FAQs on What is the Thumb Rule of 50 30 20 in Personal Finance

Q1. What is the thumb rule of 50-30-20 in personal finance?

It’s a budgeting method that divides income into 50% needs, 30% wants, and 20% savings.

Q2. Is the 50-30-20 rule realistic in India?

Yes, but adjustments may be needed in high-cost cities. Some shift to 60-20-20 or 50-20-30 depending on lifestyle.

Q3. Can students or part-time earners use the 50-30-20 thumb rule?

Absolutely. Even small income streams can be divided proportionally to build savings habits early.

The What is the Thumb Rule of 50 30 20 in Personal Finance is a simple yet powerful way to organize your money. By dividing income into 50% for needs, 30% for wants, and 20% for savings and investments, it offers a balance between security and enjoyment.

Unlike complicated budgets, this rule is easy to remember and apply, which makes it ideal for beginners or anyone looking to bring order to their finances.

What makes this approach effective is its balance. Needs cover essentials like rent, food, and bills. Wants allow you to enjoy life without guilt. Savings create your future security through emergency funds and investments. This mix ensures you’re not only surviving today but also preparing for tomorrow.

Of course, personal circumstances vary. In high-cost cities, needs may take up more than 50%, and that’s fine – the percentages can be adjusted.

The important part is to develop the habit of consciously dividing income rather than spending without a plan. Even if you start with smaller savings, consistency is what builds financial strength over time.

The rule also reduces financial stress. Instead of wondering where your salary disappeared, you have a roadmap. That clarity builds confidence, giving you control over money rather than letting money control you.

In short, the 50-30-20 thumb rule is not a rigid formula but a guiding principle. It helps you balance responsibilities with lifestyle choices while ensuring steady savings.

Whether you’re a student, professional, or family, adopting this rule can create a healthier financial life. Start small, stay consistent, and let these three simple numbers 50, 30, and 20—guide you toward long-term financial well-being.

Table of Contents

Read more:

What Is a Simple Way to Save Money? 7 Easy Habits That Actually Work

How to Create Passive Income in India: Complete Guide for 2025

Disclaimer: The "What is the Thumb Rule of 50 30 20 in Personal Finance" article is for educational purposes only and should not be taken as financial advice.

3 thoughts on “What is the Thumb Rule of 50 30 20 in Personal Finance?”